That jab in the nose hurt! SPX dropped $35 or 1.7% to close at $2044. SPX didn't even hesitate at the 50 dma at $2061. RUT lost $15 or 1.2% today, closing at $1208. $1210 was the high reached twice in 2014 by RUT and that level also served as resistance in early February before RUT took off to set new all-time highs. RUT's 50 dma is at $1203, but this market may give back more than that before it is done. Volatility is starting to heat up, with the VIX gaining 1.6 points today to close at $16.7%. That places us back in the range of volatility from the choppiness we endured in January.

Conventional technical analysis would conclude from today's price action that we are now back in that choppy range from January, roughly $1990 to $2065. The 200 dma is at $2001, just above that support level at $1900. Today's price takes us down 3.4% from the high on March 2nd. If you follow Fibonacci retracements, the 62% retracement level is at $2034 on SPX. I have not used Fibonacci much myself, but I have been surprised how often those numbers seem to arise. That $2034 level would be a 4% correction, similar to what we saw in mid-December and early January. In any case, all one can do is mark some points where positions must be adjusted or closed, watch what the market gives us each day, and take appropriate action.

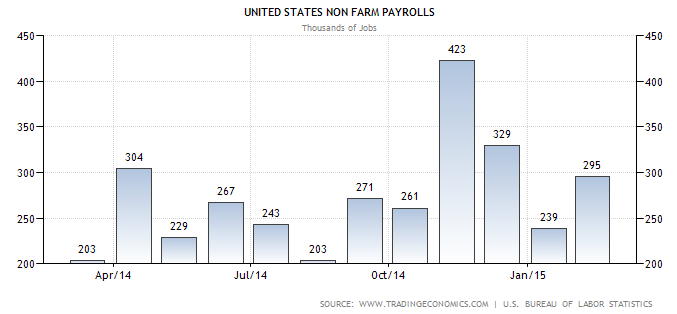

The conventional wisdom for this correction appears to be the "unusually good" jobs report causing traders to expect increased interest rates from the Fed sooner than expected. I explained why I thought that unlikely yesterday, but I found a nice graphic illustrating the problem. In the chart below of the non-farm payroll numbers for the past 12 months, it is hard to see the February number as "unusually good". In fact, it's hard to identify a trend. But I received that headline on my phone from Yahoo Finance as the explanation for this market pull back, so it must be true.

My March iron condor position on RUT stands at a net gain of 2% (increased implied volatility pulled it back), and delta for the position equals +$57 and position theta = +$229. Delta of the short $1060 puts = 12, so we are pretty safe at this point. We will hit our two sigma rule Friday, so we may be closing the put spreads then if not before. The April condor is delta neutral (position delta = +$19 on 20 contracts) and is showing a small gain of 1% at this point. Hold on for the ride!